TRON founder escalates feud with Trump-linked DeFi project, alleging coercion and frozen voting rights.

World Liberty Financial’s freshly posted governance proposal to unlock 62.3 billion WLFI tokens drew an immediate broadside from TRON founder Justin Sun, who published a lengthy rebuttal on X, calling the plan “World Tyranny, Not World Liberty Financial.”

Sun, who invested $75 million in the Trump family-backed DeFi venture, accused the team of engineering the vote so that dissenters are punished, as holders who vote against the proposal see their tokens locked indefinitely with no unlock path, while large holders like himself have been frozen out of the process entirely.

“I personally hold approximately 4% of the voting power, yet my tokens have been frozen and I am forced out of this voting process,” Sun wrote. “The outcome was determined before the vote even began.”

The proposal, announced by WLFI on Tuesday, would place early supporter tokens on a two-year cliff followed by a two-year linear vest. Founders, team members, and advisors would face a longer five-year schedule, with 10% of their allocation permanently burned on passage. Holders who do not opt in remain locked indefinitely. WLFI called the plan “one of the strongest long-term governance alignment signals in DeFi.”

Sun sees it differently. He called the vote “a performance where the police have already barricaded the doors of parliament” and pointed to what he described as a deeper structural problem: the WLFI smart contracts are ultimately controlled by a 3-of-5 anonymous multisig and a single anonymous guardian address that can blacklist any wallet. Voters, meanwhile, must complete identity verification to participate.

“Your voters must register, submit to scrutiny, and be vetted — while your dictators won’t even show their faces,” Sun wrote.

Feud Erupts Into Open War

The response caps a week of escalation between the two sides. Tensions boiled over on Sunday after Sun accused WLFI of embedding a hidden blacklisting function in the token contract and called the team’s actions illegitimate. WLFI fired back, threatening legal action. “See you in court pal,” the project’s official X account posted.

Sun demanded that whoever was operating the account identify themselves. “As the largest investor in this project, I demand that those responsible come forward by name, instead of hiding in the shadows.”

The clash followed days of scrutiny over WLFI’s treasury operations. The Defiant previously reported that WLFI deposited 5 billion of its own governance tokens into Dolomite, a lending protocol co-founded by WLFI’s chief technology officer, and borrowed roughly $75 million in stablecoins, some of which were routed to Coinbase Prime.

Sun’s wallet containing more than 500 million WLFI tokens has been frozen since September 2025, when the project blacklisted his address after on-chain analysts flagged transfers routed through HTX, his crypto exchange. WLFI alleged Sun breached his investor agreement. Sun has maintained that the freeze was unjustified.

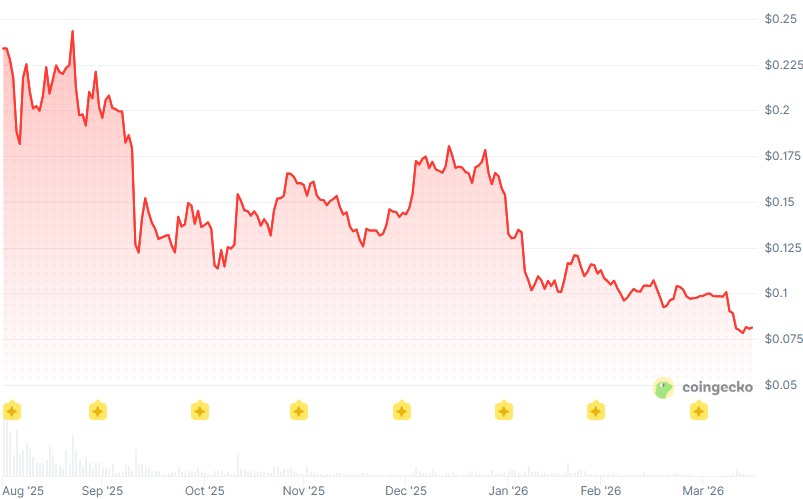

Token in Freefall

WLFI was trading around $0.08 on Tuesday, down roughly 75% from its all-time high and near its all-time low of $0.077 hit last week. The token’s market cap has fallen to approximately $2.5 billion.

Sun closed his statement by calling on all WLFI holders to “see this proposal for what it truly is” and to “reserve all legal rights of recourse.”

This article was written with the assistance of AI workflows. All our stories are curated, edited and fact-checked by a human.